The United States is currently utilizing its position as the world's largest exporter of Liquefied Natural Gas (LNG) not merely as a commodity play, but as a strategic anchor in a high-stakes trade negotiation with the European Union. This maneuver transforms a bilateral energy dependence into a conditional asset, where "favourable access" is no longer a market default but a negotiable concession. Understanding the mechanics of this pressure requires a granular look at the infrastructure of the global gas market, the specific legal triggers of US export authorizations, and the structural vulnerabilities within the EU’s energy transition.

The Triad of US LNG Leverage

To quantify the current threat to EU energy security, one must examine the three distinct levers the US executive branch can manipulate to alter the flow of gas.

1. The Public Interest Determination Bottleneck

Under Section 3 of the Natural Gas Act, the US Department of Energy (DOE) must determine whether exporting natural gas to a country without a Free Trade Agreement (FTA) with the US is "consistent with the public interest." Because the EU does not have a comprehensive FTA with the US, every molecule of LNG shipped to European terminals is subject to this discretionary oversight. The US can effectively throttle future supply by simply extending "pauses" on new export permits, citing domestic price stability or environmental impact assessments. This creates a non-tariff barrier that functions as a political dimmer switch.

2. Destination Flexibility vs. Long-Term Commitment

The primary value proposition of US LNG has historically been its lack of destination restrictions. Unlike Qatari or Russian gas, which often comes with "point of delivery" clauses, US cargoes can be traded on the spot market. By signaling a move toward "favourable access," the US is suggesting a tiered system where specific allies receive priority in terminal scheduling or regulatory fast-tracking, while others are forced to compete in a more volatile, high-priced global auction.

3. Infrastructure Financing and De-risking

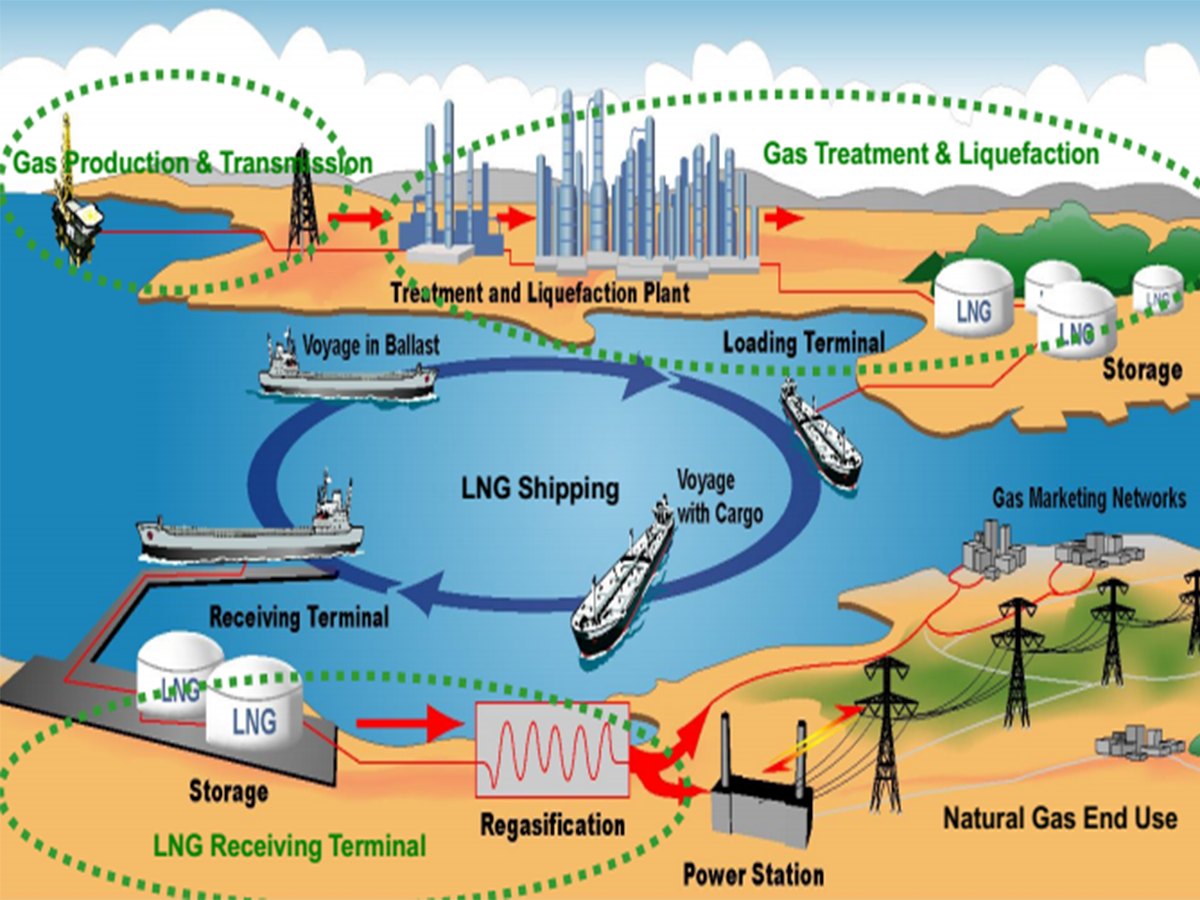

The expansion of US export capacity—specifically the "Second Wave" of Gulf Coast projects—requires Final Investment Decisions (FIDs) backed by 20-year Sale and Purchase Agreements (SPAs). If the US government creates a climate of regulatory uncertainty regarding exports to Europe, European utilities will find it impossible to secure the financing necessary to build receiving infrastructure. This freezes the EU’s ability to further diversify away from pipeline gas.

The EU Cost Function: Why Alternatives are Failing

The European Union’s vulnerability is rooted in a fundamental mismatch between its decarbonization goals and its immediate baseload requirements. The "Risk of Losing Favourable Access" translates into a measurable increase in the Levelized Cost of Energy (LCOE) across the continent.

- The Pipeline Deficit: With the destruction of the Nord Stream system and the steady decline of Norwegian Continental Shelf output, the EU has lost its buffer. Pipelines provide continuous flow; LNG provides "lumpy" delivery. Managing this "lumpiness" requires massive investment in regasification units (FSRUs) and storage, costs that are only amortized if supply is guaranteed and cheap.

- The Global Bidding War: Without a trade deal that secures US preference, the EU enters a direct price war with the JKM (Japan Korea Marker) buyers. Asian demand is structurally more resilient because of higher industrial margins and a slower transition to renewables. In a pure market-clearing scenario, EU industry—specifically German chemicals and heavy manufacturing—cannot sustain the $15–$20/mmBtu price points that Asian utilities can absorb.

- The Green Hydrogen Gap: While the EU hopes to pivot to hydrogen, the technology remains at a low TRL (Technology Readiness Level) for mass industrial scale. LNG is the only bridge fuel that fits existing infrastructure. Removing "favourable" US access effectively burns the bridge before the destination is reached.

The Logic of the Trade Linkage

The US demand for a trade deal—likely involving agricultural concessions, reduced tariffs on American vehicles, and digital services parity—uses energy as a "loss leader." The US is betting that the political cost of high energy prices in Europe is greater than the political cost of admitting American chlorinated chicken or lowering barriers for Big Tech.

This creates a Dependency Trap:

- Step 1: Force the EU to decouple from Russian gas (completed).

- Step 2: Become the primary substitute supplier (completed).

- Step 3: Introduce regulatory friction to the substitute supply to extract concessions in unrelated sectors (current phase).

The mechanism of "Favourable Access" would likely take the form of an Executive Order or a specific DOE carve-out for "Strategic Partners," effectively granting FTA-level certainty to the EU without a formal treaty. This is a powerful carrot, but the stick is the immediate "un-favouring" of European orders in the event of a trade stalemate.

Structural Limitations of the US Strategy

The US cannot execute this threat without incurring domestic and geopolitical costs. The strategy is limited by three primary factors:

- Contractual Integrity: Much of the US LNG is already under long-term contract with private entities (Shell, TotalEnergies, BP). The US government cannot simply "turn off" existing flows without triggering force majeure litigation that would devastate the reputation of the US as a stable trade partner. The leverage is almost entirely focused on incremental capacity and renewals.

- Producer Incentives: US gas producers in the Permian and Appalachian basins require high export volumes to maintain drilling profitability. If the US government restricts exports to the EU to play hardball, and Asian demand doesn't compensate, domestic prices could collapse, leading to a domestic economic slowdown in energy-producing states.

- The Fragility of the Atlantic Alliance: Weaponizing energy against an ally during a period of heightened geopolitical tension (Ukraine, China) risks a permanent strategic rift. The EU could retaliate by accelerating trade deals with Mercosur or China, or by implementing "Carbon Border Adjustment Mechanisms" (CBAM) specifically targeted at high-methane-leakage US gas fields.

Evaluating the Risks of Strategic Inaction

For the EU, refusing the trade deal results in a "High-Beta" energy future. This involves a total reliance on the global spot market, where a single cold winter in Shanghai or a strike at an Australian liquefaction plant could trigger a recession in the Eurozone.

The US, meanwhile, faces a "Credibility Discount." If it proves that energy security is a contingent favor, it incentivizes the EU to prioritize "Energy Sovereignty" at any cost, which includes massive subsidies for domestic nuclear and renewable projects that will eventually eliminate the need for US gas entirely.

The immediate tactical move for European energy procurement officers is to move away from short-term spot purchases and toward "Equity LNG"—investing directly in the liquefaction trains on the US Gulf Coast. By owning a stake in the upstream infrastructure, European firms can partially insulate themselves from the political volatility of export permits. Simultaneously, the EU Commission must decide if the preservation of its agricultural protectionism is worth the structural de-industrialization caused by unhedged energy costs.

The leverage is real, the mechanism is the DOE's discretionary permit power, and the deadline is the exhaustion of the EU’s current gas storage reserves. The trade deal is no longer about tariffs; it is a premium payment for energy survival.

Direct the European Commission to initiate a "Sectoral Energy Agreement" that decouples LNG permits from the broader trade dispute. If the US refuses this decoupling, the EU must immediately pivot to a "War Footing" on nuclear life-extensions and state-backed long-term contracts with Qatar and Nigeria to dilute the US market share and neutralize the leverage.